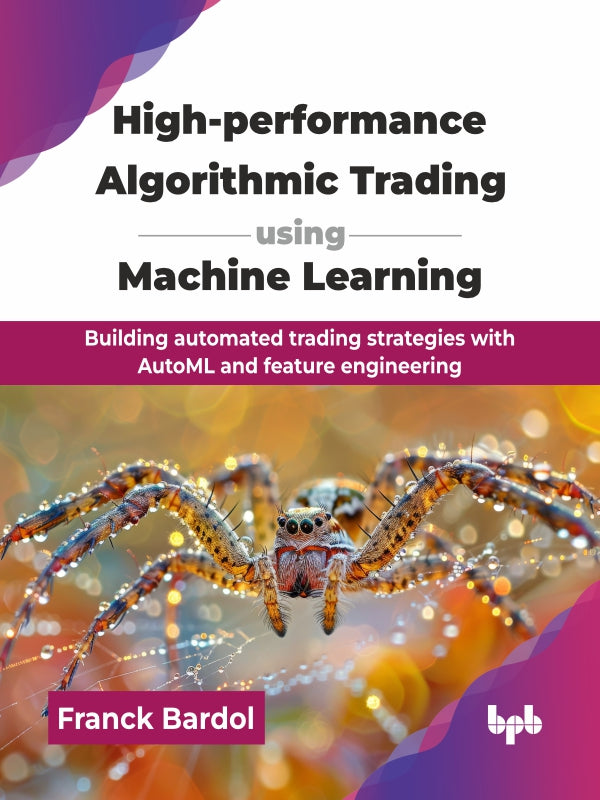

High-performance Algorithmic Trading using Machine Learning

{kind=link}

ISBN: 9789365893892

eISBN: 9789365892949

Authors: Franck Bardol

Rights: Worldwide

Edition: 2025

Pages: 340

Dimension: 7.5*9.25 Inches

Book Type: Paperback

DESCRIPTION

TABLE OF CONTENTS

ABOUT THE AUTHORS

High-performance Algorithmic Trading using Machine Learning

Sale priceRs. 1,099

Choose options

High-performance Algorithmic Trading using Machine Learning

Sale priceRs. 1,099